March, 2026

Authored by Daniele Fattibene (ETTG), Iliana Olivié (ETTG), Judith Arnal (Real Instituto Elcano), Jorge Cantallopts (Centro de Estudios del Cobre y la Minería), Claude Kabemba (Southern Africa Resource Watch) and Poorva Karkare (ECDPM)

The global energy transition has placed critical minerals – lithium, cobalt, copper, and nickel among others – at the absolute center of the geopolitical and economic map. This shift comes at a moment of unprecedented demographic pressure: over the next decade, 1.2 billion young people will enter the global labor market, yet the world economy is currently on track to create only 400 million jobs. This would leave a staggering gap of 800 million young people at risk of being excluded from the labor market. Nowhere will this challenge be more visible than in Africa, as about 350 million of those young people will be living in the Continent. Against this backdrop, the European Union’s green and digital transitions agenda are fundamentally dependent on a secure supply of Critical Raw Materials (CRMs). CRMs are essential for manufacturing batteries, electric vehicles (EVs), wind turbines, solar panels, and other clean energy solutions and the International Energy Agency’s “Global Critical Minerals Outlook 2024” reveals that the demand for lithium may increase nearly and the demand for graphite will almost quadrupling in less than 15 years.

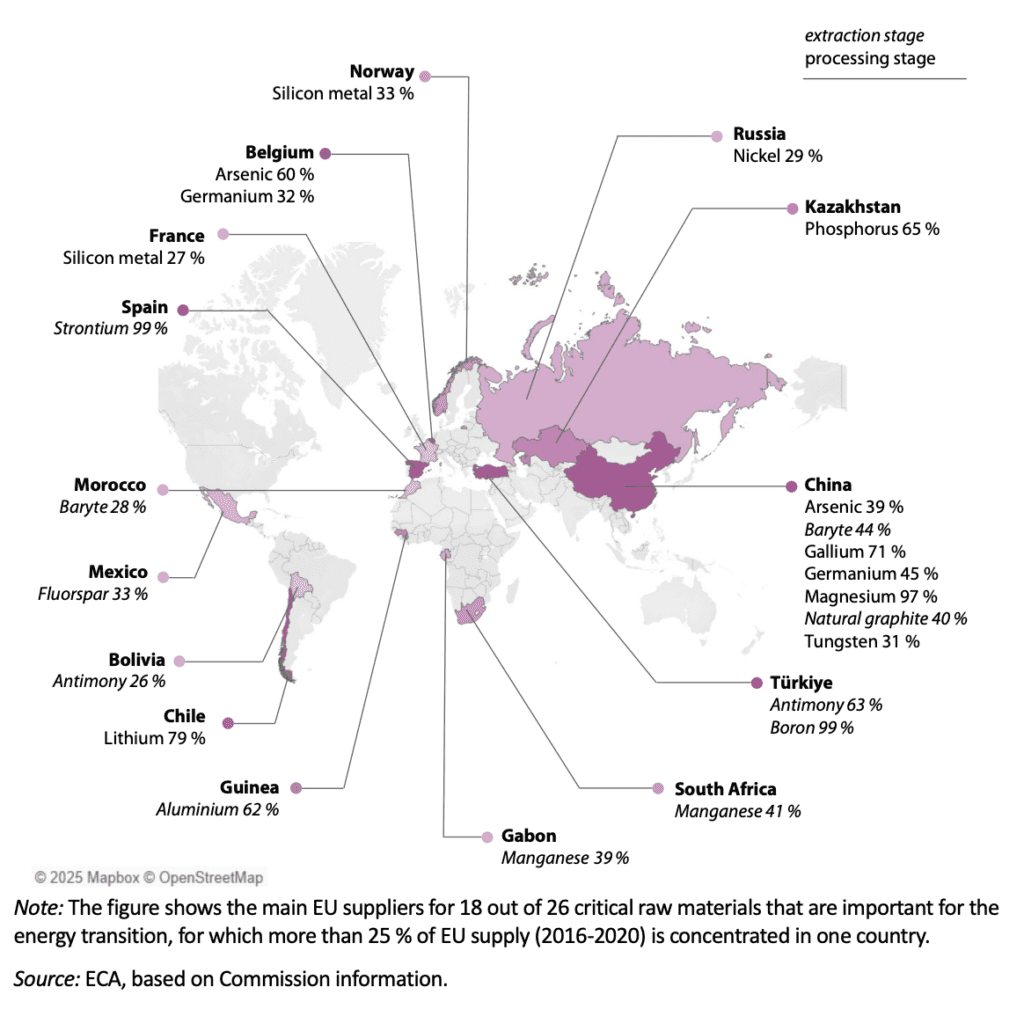

These materials form the bedrock of the EU’s industrial competitiveness, climate leadership, and strategic autonomy, yet they need to be imported from external markets and the refining is highly concentrated. A recent report by the European Court of Auditors shows that China provides 97% of the EU’s magnesium (used in hydrogen-generating electrolysers) and Türkiye provides 99% of the EU’s boron (used in solar panels). In a webinar co-convened by the European Think Tanks Group (ETTG) and the World Bank, a panel of experts from Africa, Europe and Latin America explored how to ensure the increasing demand of CRMs doesn’t repeat the “resource trap” of the past, but instead serves as a catalyst for “job-rich” growth through industrial ecosystems and economic corridors.

Figure 1: Main EU suppliers of selected critical raw materials

Going beyond the “Enclave” Economy: lessons from Chile and Africa

During the webinar, panelists highlighted that resource-rich countries, particularly in Africa and Latin America, have often functioned as sort of “enclave economies”. Minerals are extracted in raw form and exported to processing and refining hubs (especially China or in a more limited way Europe), fuelling an extractivist model based on mining, that has generated limited jobs, while creating high added value outside the countries of origin. This model has not allowed the harnessing of the full potential of those economic corridors — the energy systems, transport networks, and supplier industries – that grew around the mining sector. During the event, doubts emerged on whether the current global economic model is actually capable of delivering benefits and industrialisation to resource-rich countries. Although the energy transition debate has progressively shifted from “access to energy to power industries” and towards “structural economic transformation,” the underlying power relations remain unchanged. Despite these hurdles, the webinar showcased that Africa and Latin American countries (i.e. Chile) can offer important lessons learned to foster a paradigm shift.

In Chile, the mining sector has evolved into a highly sophisticated, knowledge-intensive sector, contributing approximately 18% directly to the national GDP. The sector, led by copper (24% of global production) and lithium (second-largest producer in the world), accounts for over 55% of total Chilean exports, and it employs over 200,000 people, offering salaries 70% higher than the national average. In this context, Chile has developed a strong ecosystem of specialized suppliers in engineering, digital technology, and water management (essential due to water scarcity in northern Chile), and many of these companies now export their services globally. The success of the sector relied not just on the abundance of these resources, but most importantly on clear rules and efficient permitting, which Chile is currently working to maintain as it updates its regulatory framework. Job creation linked to the CRM sector will come, necessarily, from indirect employment, given the low labour intensity – and high capital intensity – of the extractive sector. In this sense, building a productive ecosystem around it is essential for creating jobs, while highly qualified jobs will come from the technological sophistication of the sector at large.

In Africa, the picture gets obviously more nuanced and diversified, depending on the countries analysed. However, during the event experts agreed that the current focus of the political debate is mostly seeking to address the need to break the cycle of extraction through a series of development linkages. First, for African producing countries, it is essential to strengthen the local supply chain for mining operations (e.g., local machinery and maintenance). Although previous estimates that Africa currently holds approximately 30% to over 30% of the world’s known critical mineral reserves are increasingly challenged by other studies, there is an overall agreement that the Continent still captures less than 1% of the value generated from the manufacturing of clean energy technologies (e.g., batteries, solar panels, wind turbines). Second, it is pivotal to leverage big regional infrastructure projects such as the Lobito Corridor (linking Angola, Zambia, and the DRC), in a way that generates economies of scale with a multitude of diverse supply chains such as agriculture and agro-processing, rather than just serving as a conveyor belt for raw minerals to the coast. Thirdly, a consistent strategy of economic transformation led by the CRM sector requires to have the basics in place: adequate infrastructure, but so does a stable and affordable energy supply. Finally, the lack of coordination among African countries exposes them to aggressive trade deals that undermine regional industrialization goals. Therefore, speaking in an as much “coordinated voice” as possible is essential to seize the immense opportunities linked to mineral beneficiation across the whole continent.

The European Perspective: Strategic Autonomy vs. Development

Europe’s engagement with critical minerals is increasingly shaped by the Critical Raw Materials Act (CRMA) and the Global Gateway strategy. However, significant internal and external frictions remain. On the internal side, European mining laws at the level of Member states are severely outdated (e.g. in Spain the law dates back to 1973), while the social acceptance of this sector remains low, with local communities often litigating against new projects due to a lack of “mineral literacy”. On the external side, there is a clear divergence between the EU’s approach to minerals, compared to its partners. While the EU sees CRMs through the lens of “economic security” and “strategic autonomy,” partner countries view them as a tool for “industrial development” and creation of solid and sustainable supply chains with high added value. In addition, it does not appear realistic that the EU will outpace Chinese competitors in the short-term, as they currently dominate processing and refining, after years of investing in key value chains starting from electronics and batteries upward. Hence, to compete the EU could focus more on trilateral cooperation—for instance, incentivizing Chinese refining operations to relocate to Africa where they can be supported by European infrastructure and sustainability standards. A recent analysis on the Democratic Republic of Congo outlines a scenario on the cobalt supply chain in which the EU could fund infrastructure, training and Environmental, Social, and Governance (ESG) support, while China invests in refining via a joint venture with local suppliers, and the refined cobalt could be supplied to a Sino-European venture based in Europe to produce downstream products, including EV batteries.

Working on Win-Win partnerships

The event concluded with several concrete steps to bridge the gap between resource extraction and job-rich growth. First, it is important to differentiate the minerals. While the EU focuses on rare earths, developing countries find copper, iron, and aluminum more “critical” because their larger markets generate more income. Second, Africa could develop its own ESG framework that external partners must abide by, reducing the confusion caused by a “multiplicity of frameworks”. Third, considering the long timelines of mineral projects, public institutions need to provide better financial guarantees to ensure projects are not abandoned due to short-term market fluctuations. Fourth, since around 60% of mining-related jobs are for technicians, engineers, and mechanics, it is crucial to unlock higher investments in technical education, to avoid that these jobs will continue to be filled by foreign workers and to carry out effective local capacity building and knowledge transfer. Finally, as mining ministries cannot work in isolation, a true industrialization requires a strong alignment of trade, energy, and transport ministries to ensure minerals support broader goals like food security and regional trade.

The energy transition is already reshaping the global economy and geopolitics. The EU is at a strategic crossroads: either it keeps reinforcing the old patterns of extraction or it starts co-designing with partners new modalities of cooperation. Research – rich countries have the potential to build alliances with big markets like the EU to turn extraction into profitable value chains that can generate millions of skilled workers and productive jobs. As the webinar demonstrated, achieving the EU’s strategic objectives requires moving to a more comprehensive definition of what geopolitical self-interest actually means and investing in the human and industrial ecosystems that make a “job-rich” future possible.